Mastering Your 2026 Retirement Strategy: A 16-Step Annual Roadmap

If you’re a U.S. employee, the start of the year usually brings one big financial question to the top of your mind: How should I be saving and investing for retirement right now? A viewer asked this question on one of my videos last year and so I thought I’d share how my strategy for this built over the last 15 years. When you’re just starting out even the terminology can be confusing - 401k, Roth IRA, HSA, 529 plans, employer sponsored plans, and on and on.

I’ve been using this 16-step methodology for over a decade. I released a YouTube video talking about it yesterday in case you are interested (apparently YouTube doesn't like when creators link to the video directly so if you want to go see it - it's the most recent video).

While tax planning is highly personal, these "rules of thumb" will get you about 90% of the way there. I have the .pdf I walkthrough on the video under Member Tools of the site. Here's a quick link the Google Drive.

Phase 1: The Foundation (Mindset and Math)

Before you move a single dollar, you need to understand what you are optimizing for. We are optimizing for: free money from your employer if they incentivize you to save money, optimizing your taxes now (which means more money back on a tax-return, or less money paid every paycheck), and a thoughtful tax plan for your future self. Long-term planning can be the difference in hundreds of thousands of dollars, so it’s time well spent to learn (in a way, you are paying yourself for an education). One comment: tax planning is highly personal. I am always learning more in the world of finance, and the more I learn, the more I realize how different each person’s situation is. What works for me, or for most 90% of the time may not work in a specific circumstance. So take all of my steps with the understanding that you may need to tailor these steps a bit for yourself. My goal is to help provide some of the building blocks so you can configure them in a way that works for you and your unique situation.

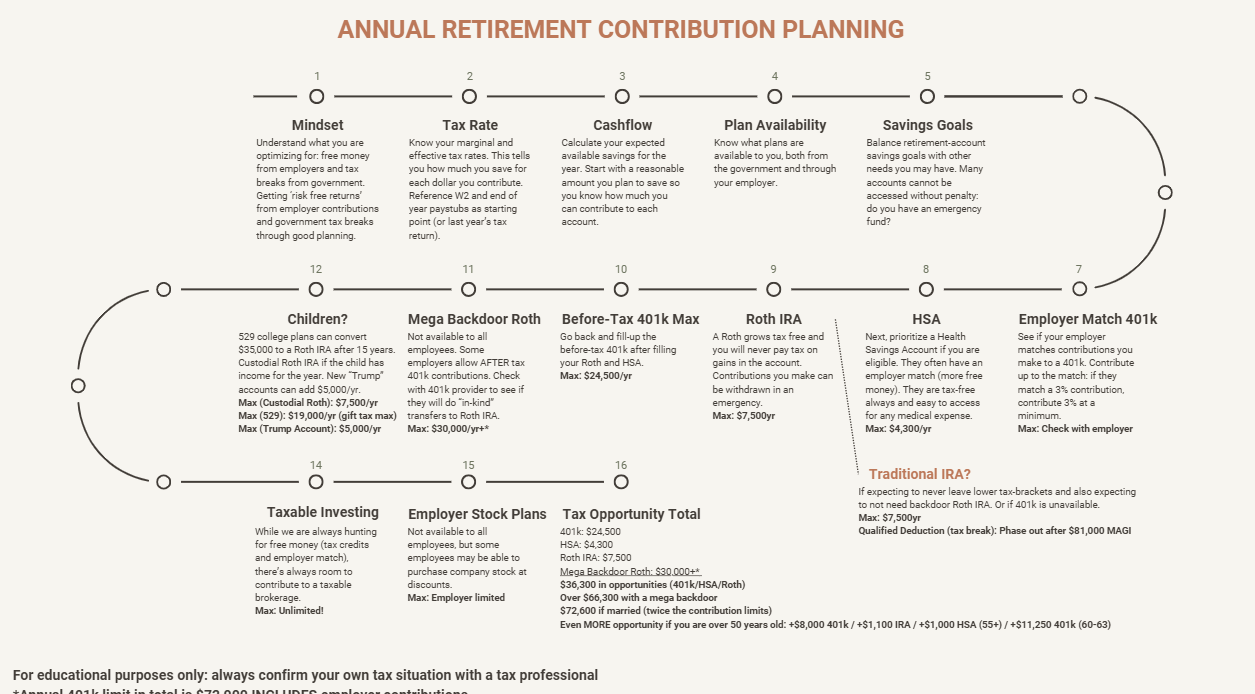

1. The Mindset

The biggest mindset shift I had was beginning to look at all “Retirement” accounts as simply tax-advantaged accounts that I can play with to make more money. I stopped thinking about “Retirement” as some far-off thing, and thought more about how to use the tax-code to my advantage now and into the future. I was looking for ‘free’ money and all I had to do to get this reward is pay myself first by saving money. This seems like a small point and it is subtle, but you would be surprised that many people don’t even know what investments sit in their 401k account - or even worse - never invest at all in these accounts.

2. Know Your Tax Rates

The next part is understanding how much you are actually paying in tax - what is your effective tax rate and marginal tax rate. These are dry, boring tax terms that play a big role in how much money you make and keep every year. And when your money compounds in investments - play an even bigger role down the road when you are looking to spend your investments down. One thing I didn’t mention in this week’s video: there is a LOT that goes into calculating your effective tax rate: the standard deduction, child tax credits, and more, play a large role in reducing how much income the government looks at to tax. You should understand your marginal tax rate which is the rate you pay on your last dollar of income. In our progressive system, your tax rate goes up as you earn more.

- In the video I show an example of someone sitting in the 22% bracket: If you’re in the 22% bracket, every dollar you put into a before-tax 401k avoids $0.22 in taxes. That is an immediate, risk-free return on your money.

- See page 2 of the presentation for some additional tax detail.

3. Audit Your W-2

Look at Box 1 (Wages/Tips) versus Box 3 (Social Security wages) on your W-2. If those numbers are identical, it's a red flag that you may not be doing enough before-tax contributions to lower your taxable income.

4. Cashflow and Savings Goals

You can’t plan your contributions if you don’t know how much you realistically can save in a year (what is often called your "saving rate" - or the % of your annual income you keep for yourself). The better you get at managing cash flow and having a clear view into your annual saving plan, the more strategic you get about which retirement buckets you are targeting to fill in the year. Finally, before aggressive investing, ensure you have a "Safety Net" at least enough to cover your high-deductible health insurance or a major home repair. It doesn’t make sense to try and save a bunch at the beginning of the year in retirement accounts you can’t access, only to realize you needed some of that money for an emergency. The worst would be going into credit card debt to support spending while contributing to savings. I tricked myself at the beginning of my journey this way.

Phase 2: The Contribution "Order of Operations"

This is the specific order I fund my accounts to ensure I never miss out on incentives.

Step 6: The Employer 401k Match (The "Must-Do")

Priority #1. If your employer matches 3% or 6%, you contribute exactly that much first. This is a 100% return on your money before the market even moves. Leaving this on the table is like throwing away part of your salary. Now you may hear from people with something to sell (like a Whole Life Insurance plan)that say a 401k account is a bad account. Sure, DO check to see what the fees are for your 401k account - sometimes employers have high administration fees or limited investment options. I still have never seen a 401k account that is so bad that taking of the match is a poor decision.

Step 7: The Health Savings Account (HSA)

Next, I always max a Health Savings Account. They are incredible investment accounts and I will likely do a full video dedicated to HSAs. You need a “high deductible health plan (HDHP)”. I would often select an HDHP on purpose to be eligible for an HSA. They are typically the “bronze” plans that an employer offers. Keep in mind this starts to mix health and medical needs with finance - so you should prioritize your health first and choose the best medical plan for your unique situation. But what I found for my situation was that typically a bronze plan was much cheaper every month but you paid for it when you went to the doctor or hospital. These plans ended up costing me the same - it’s just a gold plan was a fixed monthly cost with less “lumpy” expense. You should run the math for your own available plans.

But if you DO have access to an HSA, they are your best friend. Often an employer will match your contribution up to a certain amount. You don’t pay tax on money going in, on the growth in the account, or when you take money out. Also, there’s no expiration on when you can take money out for past medical expenses. I had a surgery over 10 years ago - if I wanted to pay myself for that surgery I could take money out if I had the receipts for the surgery. Now, I never do this. Instead I pay out of pocket for medical expenses and let my HSA continue to grow.

- 2026 Max: $4,300/year.

Step 8: The Roth IRA

You will often hear debates on whether you should contribute to a Traditional IRA or a Roth IRA. It is probably the most talked about topic in retirement planning - especially as you get closer to retirement. That’s because it’s a complex decision and often based on assumptions you make about the future. What you are deciding is: do I want to NOT pay tax now (Traditional IRA or a 401k), and instead pay tax later when I withdraw money, or do I want to pay tax now and never pay tax on that money again (Roth IRA) Next, go to the Roth IRA. You pay tax now, but the growth and future withdrawals are 100% tax-free.

- I like going with a Roth here for many reasons. One, if you are new, the money you put into a Roth CAN be withdrawn at any time. You should never do this if you can avoid it, but if you “oversave” (see cashflow #4), you could withdraw some of your savings if needed.

- You are already going to be saving in a Traditional IRA: your 401k becomes a Traditional IRA when you leave your employer. So you already are filling some of the “before tax” bucket.

- When you get deeper into retirement planning, it helps to have money in different tax treatment “buckets”. You can strategically do Roth IRA conversions at times in your life when your tax rate is low. You can access Roth IRA money easier into the future and it is free from other restrictions that could impact you down the line (RMAs, beneficiary tax bombs if you leave an inheritance).

- 2026 Max: $7,500/year

Step 9: Before-Tax 401k Max

Once the match, HSA, and Roth are handled, go back and fill the rest of your 401k. As an example, let’s say you are in the marginal 22% tax rate and save the full $24,500. That would be a $5,390 savings on tax (.22 * 24500). Keep in mind, you probably will not save that much because there will be other deductions like I mentioned earlier that lower your rate already. But again, it’s free money. When I would run my taxes every year I could see where I “made” an additional $2,000-$4,000 simply for paying myself. It’s pretty cool to be rewarded for good financial decisions.

- 2026 Max: $24,500/year.

Phase 3: Advanced Optimization

If you still have money left to invest (a great problem to have!), look at these specific buckets:

- Mega Backdoor Roth: Some employers (about 5%) allow "in-kind" transfers of after-tax 401k contributions into a Roth IRA. This can allow you to shield an additional $30,000+ per year.

- Kids' Future: Use 529 plans for college (which can now convert up to $35k to a Roth IRA after 15 years) or Custodial Roth IRAs if your child has earned income.

- Taxable Investing: what about just investing in a brokerage account? Keep in mind, you will probably already have money outside of retirement accounts that you have set aside for your emergency fund or other medium term savings goals. But, there’s also nothing wrong with prioritizing a taxable investing account as long as you understand that you’re leaving money on the table in retirement accounts. This can be a strategic decision: you have full control over when you access taxable accounts (obviously, you’ve already paid tax!) This creates “optionality” for you. You pay more tax, but you get more flexibility over the money. This is a whole separate discussion that maybe I’d make a video about one day.

- A helpful rule of thumb is to think about balancing 1/3 of money in taxable accounts, 1/3 in tax free (Roth) accounts, and 1/3 of money in tax deferred (Traditional/401k accounts). Realistically, you probably won’t be able to get that much money in a Roth with annual limits. Likely you will have a larger Traditional/401k account because of the higher limits and employer match. And there’s nothing wrong with that necessarily.

Putting it all together: how much can you save?

The main point I hope to leave you with is that there is often not a limit on how much you can save. And these aren’t ‘super secret’ tax loopholes. They are pretty straightforward and simple if you can save into them:

- Individual: ~$36,300 in core opportunities (401k/HSA/Roth).

- Married: Over $72,600 in tax-advantaged space.

- Over 50? There are even more catch-up contributions into these accounts to take advantage of.

So that’s it! As you can tell, the individual building blocks aren’t that complicated. But it does get complex once you start customizing them for your own financial situation. Here’s the checklist I’d leave you with:

- DO have an annual plan and optimize for “free money” and tax incentives.

- Understand your tax rate and what plans you are available for.

- Have a strategy for how much money you can realistically save in a year and then work backwards to filling each retirement bucket.

- In general: 401k match → HSA → Roth (or Traditional) → go back and fill 401k → explore other opportunities (mega backdoor roth, etc) → decide where to prioritize taxable investing.

Best of luck in the new year on your planning!

Member discussion