U.S. Treasury T-Bill Ladders: The Ideal Way to Manage Cash Savings?

First, an apology! It has been quite a few weeks since I last wrote a newsletter. A mix of a spring break vacation, procrastination, and being overly self-critical has put a cramp in my content output.

But, just like with money, what’s done is done, and there’s always today to start making improvements in our habits.

My next video will discuss the advantages of buying Treasury Bills directly from the U.S. Treasury for your cash savings. I received a few comments and questions on this topic, and I thought I’d share some high-level details with you in the newsletter before releasing the video tutorial.

So, what is a T-Bill ladder, and why am I considering setting one up?

The U.S. Treasury holds auctions every week to sell Treasury Bills, which are safe investments from the U.S. government that anyone can buy and typically earn an interest rate higher than a high-yield savings account or money market.

These bills take between four and 52 weeks to “mature,” which is how long you must wait before they pay you back for the purchase you made at the auction. For instance, let’s say you wanted to buy a $1,000, 4-week Treasury Bill. When you purchase it at auction, the government gives you a discount. Let me give a quick example:

At auction, instead of charging you $1,000, they might sell it for $999. In 4 weeks, they give you $1,000.

So, you would have waited four weeks, and your money would have earned $1 on its own (the $1,000 you get back in four weeks, minus the $999 you spent at auction).

The beauty of this is that when one bill matures and you get your money back, you can automatically purchase a new treasury bill. This creates a continuous loop that earns you money each time a bill matures. This can be a great way to earn money on cash you have sitting on the sidelines that you need to keep safe, while still earning money and often more than you can make in a high-yield savings account (HYSA) or money market. Let’s go through the pros:

- Risk-free: Since we depend on the U.S. government not defaulting on its debts, you are buying securities directly from the U.S. Treasury. Most large money markets hold the majority of their funds in T-bills, but one could argue that some money markets still have parts of their funds that are not directly from the U.S. Treasury. Here, you go straight to the source. These bills are backed by the full faith and credit of the Treasury, similar to how banks are backed by FDIC insurance.

- Tax-advantaged: Unlike a high-yield savings account (HYSA) or money market, by default, a Treasury bill pays no state or local income tax. Depending on where you live, this can save you a bit of money. They still have to pay Federal income tax, just like any interest you are paid on any investment.

- Higher Interest: Interest rates are constantly changing, but I consider Treasury rates the “standard.” What banks or other institutions offer on cash is typically less than the Treasury rate. There is a lot of nuance on this point, but in general, T-bills will earn higher interest on your cash, which I’ll discuss later.

- No Fees: this is a big one! You will always pay a fee, whether you see it or not, to earn interest at a bank or money market. Call it what you want, but if you earn less than the rates you could be getting on a Treasury bill, you are losing money. Now, earning less is not necessarily a bad thing. You are getting added convenience and services, which is what we pay a business for. But if you want to squeeze out just a little bit more interest, T-Bills are great.

- More Liquid: You can always liquidate your treasury bills before they “mature”. Say you needed to sell your 4-week treasury bill early, you could do that. This carries some risk, as the treasury bill can be priced at whatever interest rates are at the time, so there may be a chance you make less than you locked in at auction. But, it is still more liquid than a CD, which often has strict requirements on when you can access the money.

- Autopilot/Automation: You can create what is called a “rolling” ladder with your T-Bills. The idea is that when one T-Bill reaches maturity, your brokerage can automatically buy another T-Bill. This creates a rolling effect, where you automatically buy and sell these bills, earning interest on the cash you have as a safety net.

- Customizable durations and redemption periods: T-bill durations, which indicate how long it takes for the bill to mature, come in various weekly options. The Treasury sells bills with durations of 4 weeks, 6 weeks, 8 weeks, 13 weeks, 17 weeks, 26 weeks, and 52 weeks. You also obviously have control over when you decide to buy these bills. Let’s do a quick example. Say you wanted to keep a 6-month emergency fund in T-Bills:

- You could split your purchases into four parts: week 1, you buy your first 4-week T-bill. In week 2, you buy your second 4-week T-Bill, and in weeks 3 and 4, it's the same.

- If you automated this, starting in the 5th week, your first 4-week T-Bill would have matured and could be automatically replaced with a new one.

Ok, so that all sounds cool. But what are the cons? Truth be told, I have never set up a T-Bill ladder. Although as part of this process, I probably will now. 🙂

Here are the cons as I see them:

- It adds some complexity: “Let the complexity earn its place” is a recent quote that I’ve adopted. We aren’t talking about a significant difference between the interest paid on T-Bills and the interest in a money market or a competitive HYSA. However, more is always better, and if you owe state or local taxes, it could save you even more.

- You have to work to purchase them: To set up a ladder, you have to go out to an auction and buy them. Although this can be done by simply going online at the right time and buying them, it requires setting your calendar and buying them at a specific time.

- Creating the ladder can be confusing: even though it’s relatively simple in theory, you have to determine how much you want to buy, how often you want to buy, and how spaced out you want your purchases to be.

- Purchase minimum requirements: If you buy directly from the U.S. Treasury, you can buy in increments of $100. However, most brokerages require a minimum purchase of $1,000. If you are starting out, this may make it challenging to build a ladder.

- Decision paralysis: With all the different duration T-Bills, you are faced with numerous options! Do you buy a short-term 4-week bill, or a longer-term 13-week+ bill? You will hear ENDLESS opinions from talking heads on this point. Everyone is trying to read the tea leaves of what rates will do in the future, and all durations carry different pros/cons:

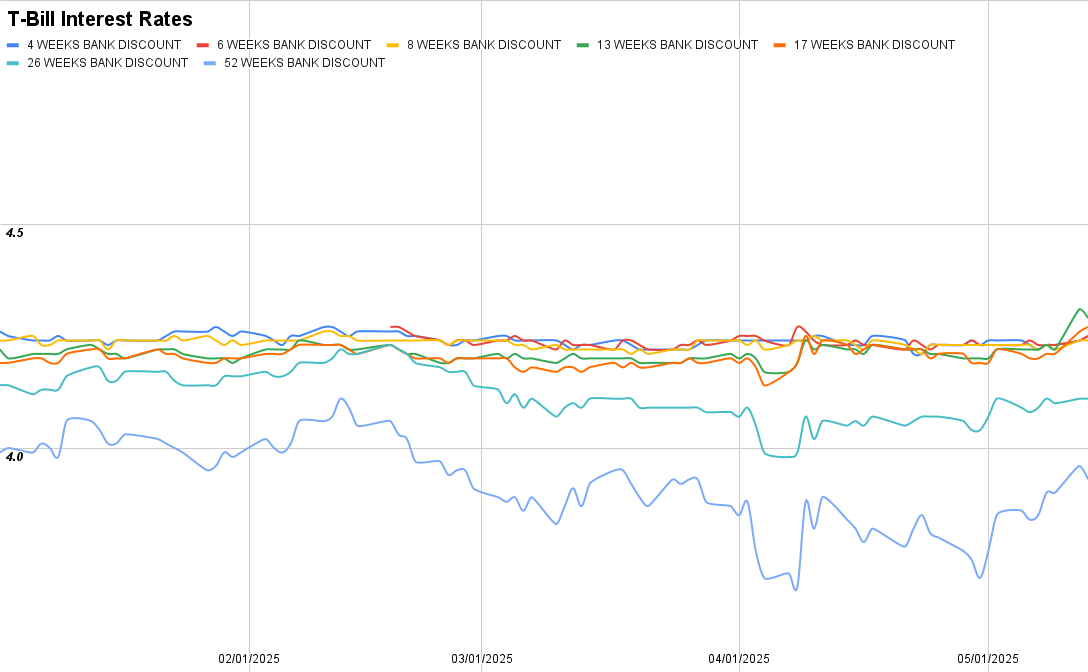

- Perhaps you want to “lock in” a rate for the long term, but what happens if the rate for that long-term purchase increases in the future? Well, the value of what you bought goes down, because people will buy the T-Bill at the new, higher rate. See the chart below for people who locked in 26-week or 52-week T-Bills that have earned less than shorter-term bills.

- What happens if you buy a 4-week bill because you don’t want to be “locked in”? Well, if rates fall, then when that bill matures, you will be forced to buy a new 4-week bill at a lower rate.

So, is it worth spending the time setting up an automated T-bill ladder? It depends. Let’s look at data I pulled from the Treasury from January to May 13th, 2025 (Daily Treasury Data).

As you can see, shorter-term treasuries have continued to stay above 4%, hovering around 4.25% between 4-week and 17-week bills. The longer-term bills (26-week and 52-week) have performed slightly worse, with a 52-week bill lagging below the 4% rate that we often hear about.

For me, I think the answer is probably “yes”, it is worth it, given all the “pros” I listed. It provides a bit of extra return for money I don’t plan to touch. It’s safe, easy to automate, and the cash can be available if I ever need it in an emergency at set intervals.

And I don’t have to worry about whether a bank will decrease my rate and force me to bank hop to stay competitive. Is there anything wrong with simply putting money into a high-yield savings account (HYSA) or money market? Certainly not. It’s simpler and doesn’t cost you THAT much. But this is a little optimization that doesn’t take a lot of time, and I enjoy doing it.

In my video, I will walk you through the process of actually placing these purchases from my Fidelity brokerage and automating re-purchases.

That is all there is to getting started with T-Bills! If you have practice purchasing or setting up a T-Bill ladder, I'd love to hear your experience!

Member discussion